Curve is a new generation of debit card. A “Smart Card”. Curve is not a bank nor a prepaid card. The best way to think about Curve is a card that is powered by your existing debit and credit cards. That is to say, when you pay for something with Curve, the transaction takes place between Curve and the company you’re purchasing from. Before the transaction is fully processed, Curve requests for authorisation from the underlying card that you’ve selected to power your Curve card. For those interested, a more technical and detailed explanation of this process can be found here.

Looking at the (highly simplified) diagram below, the transaction process goes from left to right and then back, right to left, along the chain.

Merchant <> Curve <> Card you chose to power Curve.

The different types of Curve card

There are three tiers of Curve card; Blue, Red and Metal which are free, £10 and £15 per month, respectively. Of course, the list of features grows as you go up the tiers.

Is Curve Blue worth getting?

As someone who writes a blog dedicated to Money, I love anything free and anything fintech. So, naturally, I signed up for the free Blue card some months ago. I was initially drawn in by the 1% cashback (applicable for up to 3 different retailers of your choosing). However, I soon lost interest when I realised the cashback feature is only available for 90 days as a Blue card customer.

I’m not someone who has loads of different cards and so no need to free up space in my wallet. Further, because I bank with Monzo, I already benefit from Mastercard network exchange rates when I go abroad. So the interbank exchange rates that Curve offer aren’t much of an appeal either.

Based on my personal circumstances, there is only really one reason for me to continue to use my Curve Blue card and that is Curve Customer Protection. In a previous post, I wrote about the protection that credit cards can offer to consumers. In short, Curve offers an enhanced version of this and, impressively, it’s applicable to transactions up to £100,000 in value.

Is Curve Metal value for money?

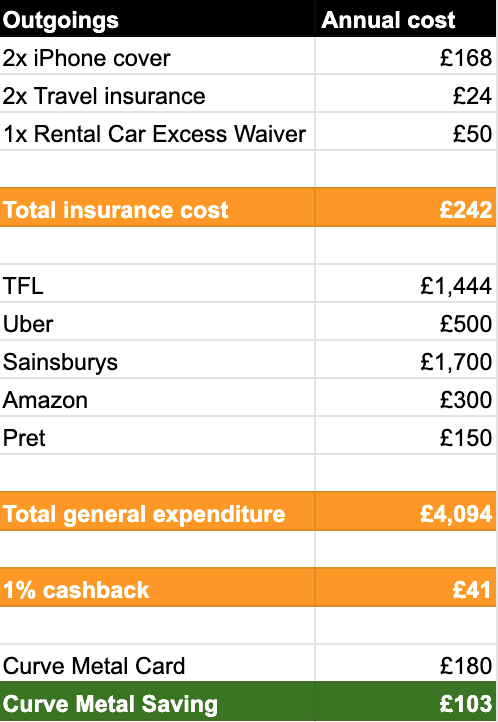

Skipping Curve Black, for now, I wanted to thoroughly evaluate Curve Metal. Metal is Curve’s highest tier card. At £15 per month (£180 / year), on the face of it, it’s a luxury product. £40 a year more expensive than the popular Amex Gold Credit Card, for the sake of example. There are two core benefits of Curve Metal: insurance and cashback. I wanted to crunch the numbers based on my own expenditure over the last 12 months. Below are the results.

As you can see, switching to Curve Metal from my current insurance providers, combined with the 1% cashback across five vendors results in a net positive £103. It is interesting to note that the cost of insuring my mobile (and my girlfriend’s) iPhones. Currently, both are insured via Protect My Bubble, the cost for this almost covers the cost of Curve Metal alone.

Gadget insurance is also a feature included in the Curve Black offering. This suggests Curve Black, at £120 / year, might be a great alternative for me. The only discernible difference between Curve Black and Curve Metal is the inclusion of the Rental Car Excess Waiver for Metal users. If you rent a car even just once a year then this might render Metal worth opting for over Black.

Curve Metal vs. Revolut, Monzo, Amex

At the time of writing, Monzo Plus is still getting its shit together after a complete flop of a launch last year (we watch this space). Revolut Metal, at £13 / month, is, in my opinion, a far below-par product to Curve Metal for a similar price. Amex’s Preferred Rewards Gold Credit Card at £140 / year is a closer contest because it includes bonus points (essentially cashback), travel insurance, amongst a few other benefits. However, it doesn’t include gadget insurance which, as we see above, can be a huge cost-saving. A major drawback for Amex cards is they are not always accepted, especially by small retailers (due to the high processing fees). Another win for Curve is that you can power your Curve Metal card with a rewards card such as the Virgin Atlantic Reward Credit Card. This means you can effectively double up on points when you transact with one of your selected vendors (up to 6 with Curve Metal),

Conclusion

The value of Curve Black or Metal depends completely on your current expenditure. You need to think about what you currently spend on insurance. Also, think about how much you could earn in terms of cashback. For this, check the list of vendors Curve partners with first. Perhaps you already have travel and/or gadget insurance included with your bank account. Crunch the numbers, as I have done above, and see if it makes sense for you!

Sign up for Curve using my referral code: TEBBS for a free £5!