Just started a new job or received a raise at your current company? Perhaps you just made the switch to being self-employed?

Then you may well be wondering “how much tax will I pay?”, and exactly how much you’ll take home each month. To find out, simply enter your annual salary below.

[CP_CALCULATED_FIELDS id=”6″]Note: the above assumes you pay Category A National Insurance. Net salary may be lower if you have a workplace pension or are paying off Student Loan.

Versus last tax year

Gladly, most people have benefited from a tax cut this year. Chancellor of the Exchequer, Philip Hammond, raised the Personal Allowance by £650 (from £11,850), and the starting point of the Higher Rate band has been revised from £46,350 to £50,000. This represents a maximum £130 tax cut for Basic Rate taxpayers, and £860 for Higher Rate taxpayers (if full Personal Allowance is applicable).

Calculating tax on income

Calculating tax on income can be a little difficult. Many people interpret the tax brackets incorrectly. For example, someone earning a salary of £60,000 would be classed as a “higher rate taxpayer” but this does not mean they would pay a flat 40% tax on their entire salary. Rather, they pay nothing on the first £12,500, 20% on £37,500, and 40% on £10,000, which totals £11,500.

To understand how this works further, read about income tax bands below…

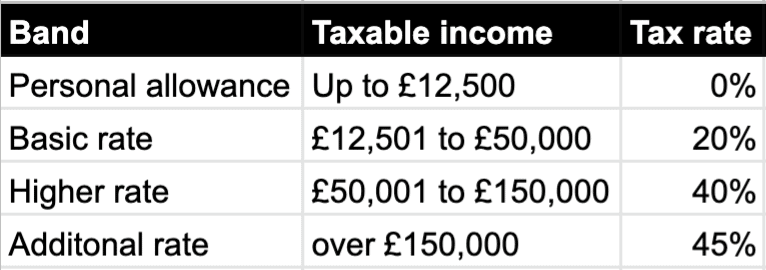

Tax bands

For this 2019/20 tax year (which runs 6th April 2019 – 5th April 2020), the government has set the income tax bands as follows.

Note that your Personal Allowance, given above as £12,500, may be more if you claim Marriage Allowance or Blind Person’s Allowance, and smaller if your income is greater than £100,000. If you earn over £125,000 then you receive no Personal Allowance.

Live in Scotland? Income tax bands in Scotland are different, albeit similar to the above.

How income tax is paid

The vast majority of people employed by a business will pay income tax as part of the Pay As You Earn (PAYE) system. Under PAYE, there is nothing for you to do as an employee. Your employer deducts income tax and National Insurance contributions from your salary and is responsible for paying this to HRMC.

HRMC will provide your employer with a tax code. This will inform your employer how much tax they should deduct from your salary as part of each pay cycle. You will receive a payslip confirming exactly how much income tax has been deducted from your gross salary. Your payslip should also clearly display your tax code. At the end of the tax year, you should is a receive a P60 detailing how much income tax you have paid in total for the year.

What is an Emergency Tax Code?

If your tax code ends with a “W1” or “M1” this means you are on an emergency tax code. This is typically due to your employer not yet receiving details of your previous income. You should have received a P45 with these details when you left your previous employer. The use of an emergency tax code is a temporary measure and you should provide details to your new employer so that they can update your tax code as soon as possible.

Self-employed

Freelancers, consultants, tradespeople and those in other professions paying their own income need to register as self-employed with HRMC by 5th October 2019. The Personal Allowance and tax brackets for self-employed people are no different from employed people, as set out above.

Remember that as a self-employed person you need to pay income tax on your profits, not your earnings.

Looking at your monthly run rate, you should attempt to calculate how much tax you will owe by the time your tax return is due. It’s important to set aside enough money each month in order to pay your income tax as part of your tax return. This tax return process is also referred to as your “Self Assesment”. You will submit two tax returns and the first has a deadline of 31st January 2020. The video below walks through how to do a tax return, step by step, and is up to date for this year. Of course, you can always pay for an accountant to do your tax return for you.

Trading Allowance

Sell on eBay, Airbnb a spare room, or generate a modest income through other means? If this is your only source of income then you will be pleased to know you do not need to do a tax return for such earnings below £1,000 as part of your Trading Allowance.

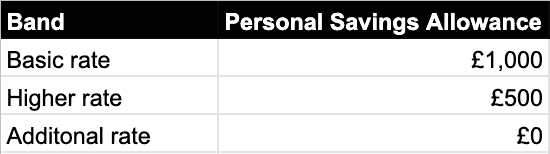

Do I pay tax on my savings?

Whilst interest rates remain miserable across almost all UK bank accounts, at least interest paid on savings can be tax-free, providing this is within your Personal Savings Allowance. Your Personal Savings Allowance is dictated by your highest tax band and is set out below.

In addition to your Personal Savings Allowance, each tax year, you are also able to put up to £20,000 into an Individual Savings Account (ISA). Interest paid on savings sitting in your ISA is never tax deductible.

Do I pay tax on my investments?

Any profit achieved on an asset, such as a second home or shares in a company, that is realised upon selling that asset, is subject to Capital Gains Tax. However, each tax year you receive a Capital Gains Tax-Free Allowance and for the 2019-2020 tax year, this has been set at £12,000.

Looking at the trading of shares specifically, any gain (profit) made above this £12,000 is subject to 10% Capital Gains Tax if your total taxable income (e.g. salary plus profit on shares sold) is within the Basic Rate bracket of income, or 20% if your total taxable income sits within the Higher or Additional brackets i.e. £50,000+.

As above, any profit on shares sold that are held in a Stocks and Shares ISA will not be subject to Captial Gains Tax and will not impact your Capital Gains Tax Allowance for the year.

Do I pay tax on my pension contributions?

Pension contributions can be subject to tax relief. This is why it can be a good idea to put as much into your pension as you can afford.

If you have opted into a workplace pension, your pension comes out of your gross salary before income tax. This means you benefit from tax relief on your pension contributions at the highest rate of tax that you pay.

The maximum you can put into your pension and still claim tax relief this year is 100% of your salary or £40,000, whichever is more.

Note that if you decide to contribute to a pension from your net salary, such as a Self-Invested Personal Pension (SIPP), then you will automatically receive Basic Rate (20%) tax relief at source. However, if you are a Higher or Additional Rate taxpayer then you will be able to claim for an additional 20% or 25%, respectively as part of your tax return.

Sources

Disclaimer: This post is for information purposes only. Whilst everything has been carefully researched and I believe it to be factually correct, I am not a trained accountant. Of course, if professional taxation advice is sought, please speak to an accountant.