Another fintech, borne out of Open Banking, Chip wants to be the best saving account in the world. However, right now in its current form, the Chip app isn’t anything special. But is all that about to change?

What is Chip?

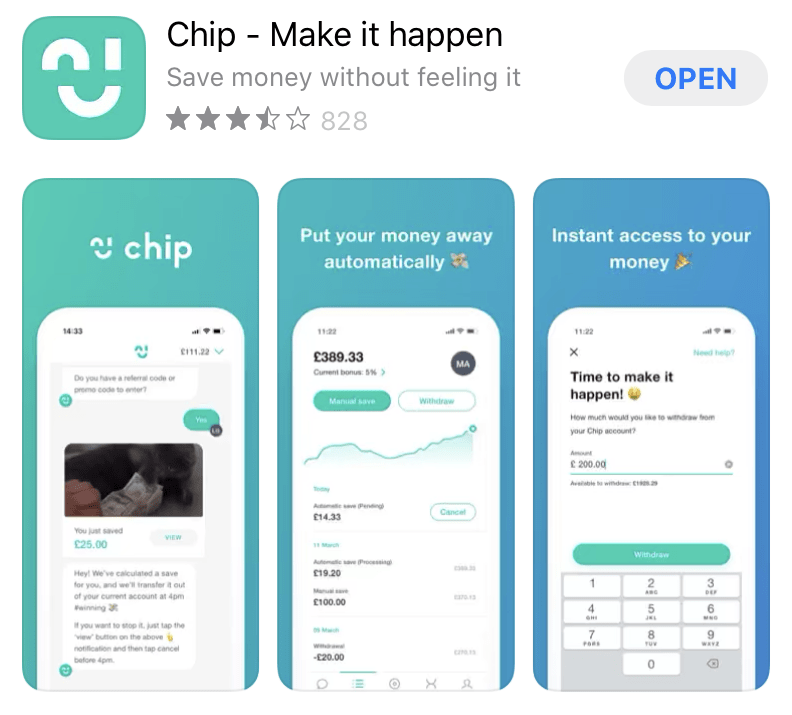

Very similar to Plum, Chip connects to your bank account, analyses what you earn, your spending habits, etc. and, based on that, automatically transfers out what it deems as appropriate amounts every 4-7 days. Chip is not a bank and has no FSCS protection, rather it uses a third-party e-wallet service to hold your money.

Except, right now, since I bank with Monzo, Chip can’t even do that. They don’t seem to have gotten around to implementing Monzo’s API, nor that of any of the other challenger banks just yet. This means the savings amounts are not accurately tailored to me, which is a huge drawback. Furthermore, at the time of writing, they are not offering any interest on my savings. All sounds wonderful so far, right?

Introducing Chip 2.0: “ChipX”

Chip has recently raised Series B funding, including £4m via Crowdcube (read about investing via Crowdcube here). This money will be used to launch “ChipX”, which will include a range of new savings products. The main one being talked about right now relates to peer-to-peer lending, which is not a new phenomenon (Zopa, for example, has been around for many years now) but Chip’s plans to leverage its customers’ spending data to inform who it lends to is what is most compelling.

There are two aspects to this. The first is that, with all the banking data that Chip has relating to each of its customers, Chip can accurately calculate risk, and hence work out which customers it should allow other customers to lend to. The second relates to the ethics of lending. How, versus the banks whose fees and rates of interest they charge customers for going into their overdraft can be astronomical (typically 15-19%), Chip is proposing a more modest 7-9%. As an individual saver, 7% is still incredibly attractive versus pretty much any other easy-access savings product. Just as important, as a borrower, that’s a lot fairer a deal too.

The question I had to ask myself is: if Chip’s customers are all looking to save then surely none of them ever use their overdraft? But, upon reflection, that’s a blinkered view. Not everyone is in the privileged position of being able to save every month. Sometimes, people only want to save for short-term goals, like to go on holiday, for example.

So I’m personally really excited for ChipX! Once launched, I’ll update this post with whether or not it lives up to my expectations.

If you enjoyed this post then you might also be interested in Three ways these fintechs might make you richer.